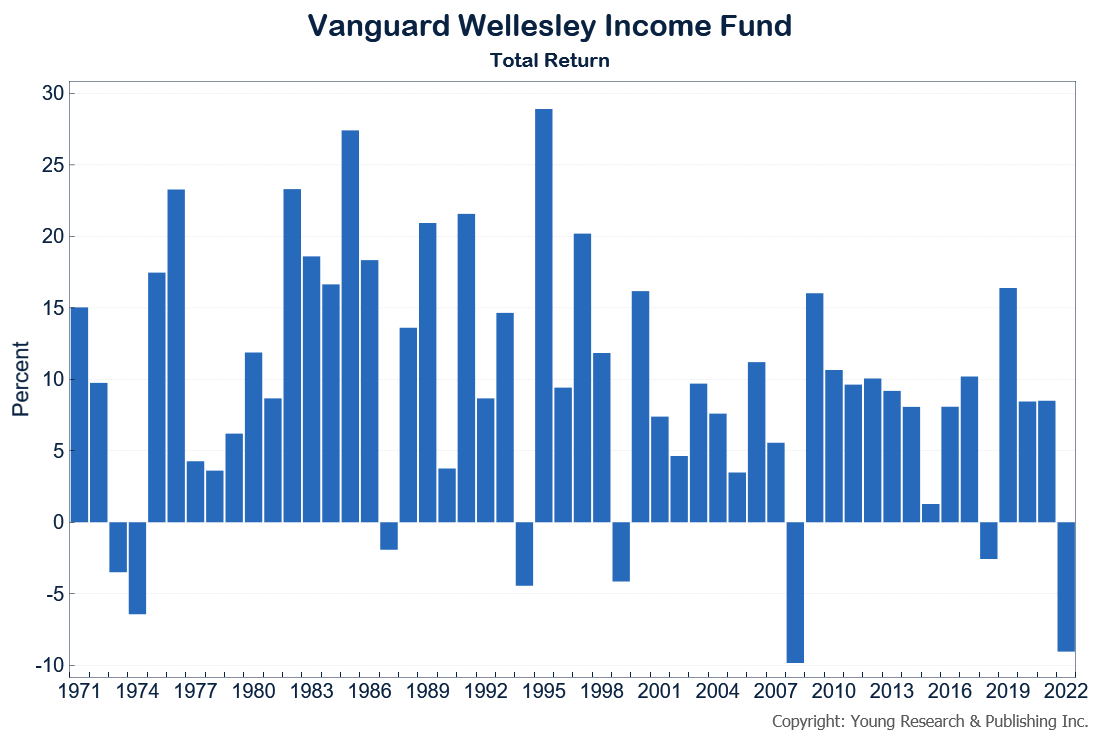

I was recently asked some questions about Vanguard’s Wellesley Income Fund by a business associate. Below is a short summary of the questions and my answers.

The first question was, “Who manages Wellesley Income Fund?”

The answer is Wellington Management Company, which I have had dealings with from my earliest days in the industry at Model Roland & Co. on Federal St. in Boston, where I began work in August of 1971. Wellington was founded in 1928 in Boston, and is one of America’s oldest institutional money managers. The two Wellington managers currently tasked with managing the Wellesley Income Fund are Loren L. Moran, who has been with the fund for six years, and Matthew C. Hand, who has worked on Wellesley for two years.

The second question about the Wellesley Fund was about how the fund is organized and diversified.

The fund is organized into bond and stock components, with 60%-65% of the fund allocated to bonds, and 35%-40% allocated to stocks. Wellington invests the bond component in “short-, intermediate, and long-term investment-grade corporate bonds, while seeking to maintain an aggregate intermediate duration.” The stock component is invested in “large-company value stocks with above-average dividends and potential for income growth.” The portfolio usually holds fewer than 100 stocks.

The final question from my associate was about Morningstar’s rating for the Wellesley Income Fund.

Morningstar has assigned a rating of five stars to the Vanguard Wellesley Income Fund. That’s the highest rating Morningstar assigns to mutual funds.