By Johannes @ Adobe Stock

Originally posted on June 16, 2026.

In 1929, Dow Jones spun out utilities from its main index and created the Dow Jones Utilities Average Index. The original components of the average were:

- American & Foreign Power

- American Gas & Electric Co.

- American Power & Light Co.

- American Telephone & Telegraph

- American Water Works & Electric Co.

- Brooklyn Union Gas

- Columbia Gas System

- Consolidated Gas System

- Consolidated Edison

- Niagara Hudson Power

- Southern California Edison

- Electric Power & Light Co.

- Engineers Public Electric

- International Telephone & Telegraph

- National Power & Light

- North American Co.

- Pacific Gas & Electric

- Public Service Co. of N.J.

- Standard Gas & Electric Co.

- Western Union Telegraph

Unlike the Dow Jones Industrials and the Dow Jones Transports, the Utilities index hasn’t been changed much since its inception. There have, of course, been consolidations and name changes along the way, but many of today’s components have roots among those from 1929. Today’s list includes (along with dividend yields as of 6.16.26):

| Company | Symbol | Yield |

| Atmos Energy Corp. | ATO | 2.36% |

| Vistra Corp. | VST | 0.56% |

| American Electric Power Co. Inc. | AEP | 2.92% |

| American Water Works Co. Inc. | AWK | 2.80% |

| Duke Energy Corp. | DUK | 3.39% |

| Consolidated Edison Inc. | ED | 3.28% |

| The Southern Co. | SO | 3.22% |

| Sempra | SRE | 2.86% |

| NextEra Energy Inc. | NEE | 2.89% |

| Public Service Enterprise Group | PEG | 3.32% |

| Xcel Energy Inc. | XEL | 3.00% |

| Edison International | EIX | 4.85% |

| Dominion Energy Inc. | D | 3.90% |

| FirstEnergy Corp. | FE | 3.90% |

| Exelon Corp. | EXC | 3.62% |

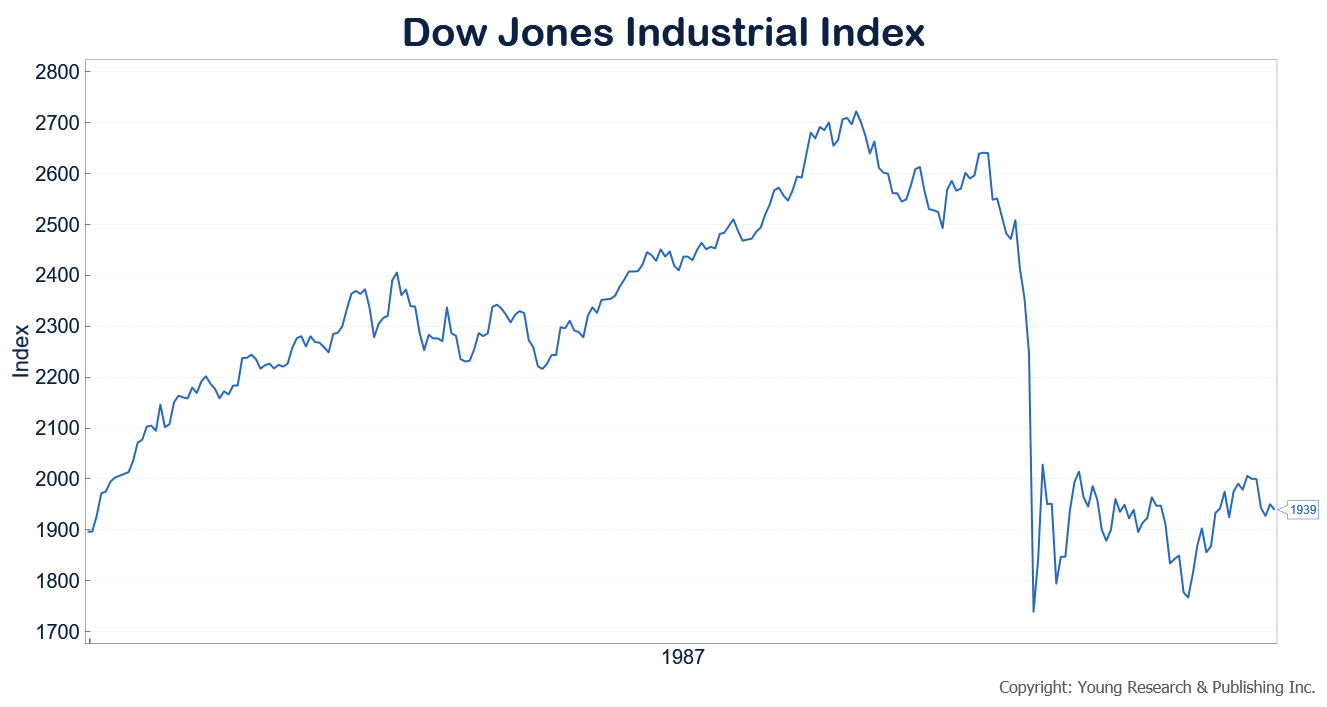

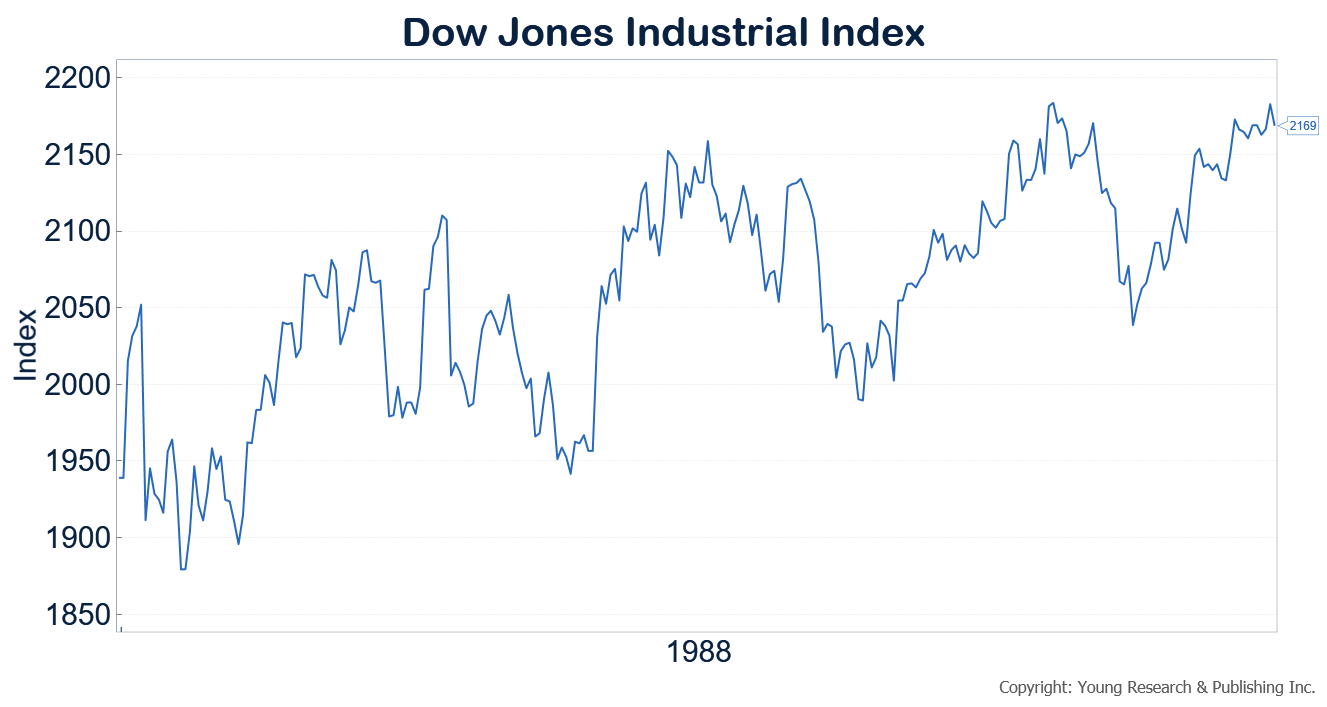

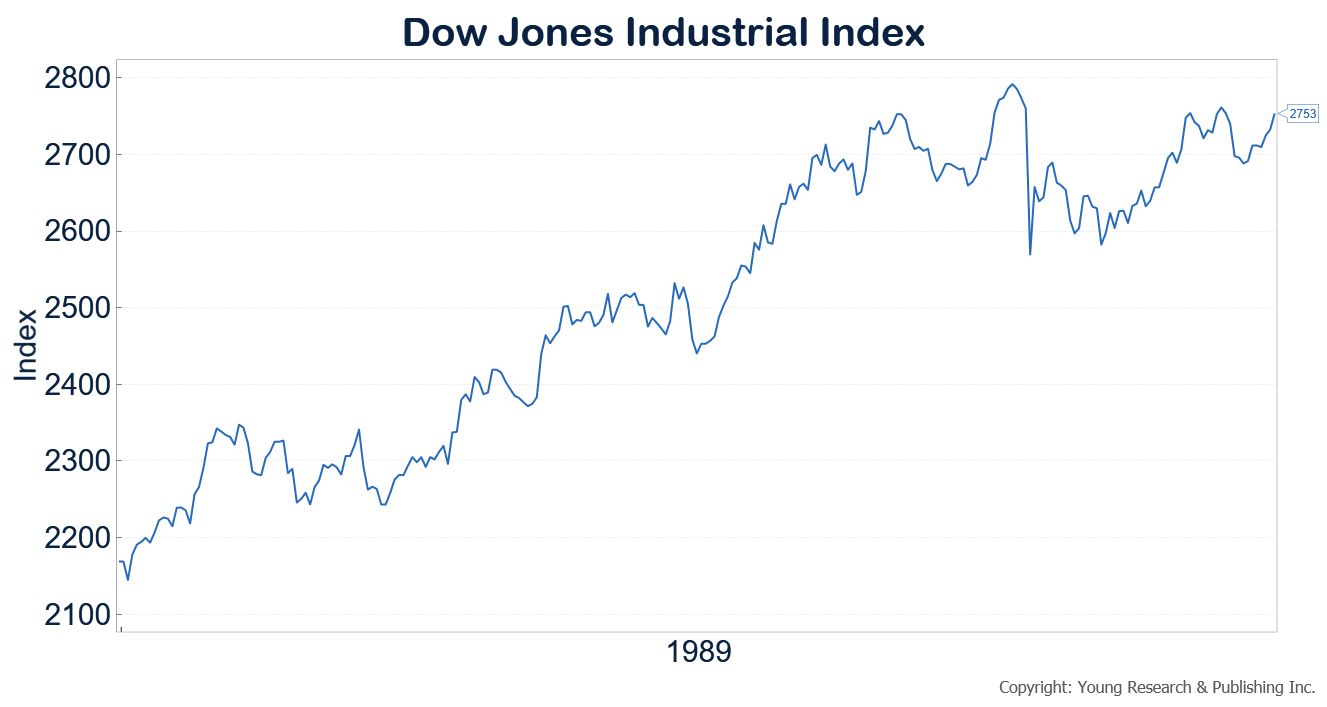

You can see that, without dividends even factored in the Dow Jones Utilities Index has grown in value through time since its inception in 1929.

But look again at the index since 1987 and compare its price return (no dividends) and its total return (dividends reinvested), and you’ll see the power of dividends and compound interest on returns.