UPDATE 6.15.26: Despite the many changes the world has seen since 2017, and all the chaos it endures today, my basic investment tenets haven’t changed. I wrote in 2017 (now itself, nearly a decade ago):

Well, writing to you now, five decades later, from our outside kitchen/living space in the heart of Old Town, Key West, I can’t help but think how much water has gone under the bridge through the many decades. But if you have been with me over the years, you are keenly aware that it is indeed the combination of dividends, compound interest, perspective and patience that frames the message I deliver to you month after month. I do not change course. You can count on it.

Originally posted April 5, 2022.

Back in 1964, I began a lifelong mission as a disciple of compound interest investing. In those earliest days, home base was Clayton Securities at 147 Milk St. in Boston’s financial district.

By 1971 I had gotten into institutional trading and research with Model, Roland & Co. on Federal Street. My first accounts were Fidelity Investments and Wellington Management.

Today, over 50 years have somehow flown by, and I am still doing business, a whole lot of it, daily with Fidelity (my family investment firm’s custodian) and Wellington (my own account’s largest positions).

Wellington, for its part, manages billions of dollars in client assets for Vanguard. In the late 80s and early 90s, my friends at Vanguard let me know that my newsletter was responsible for directing more assets Vanguard’s way than the rest of the newsletter industry combined.

Jack Bogle, the founder of Vanguard, was a friend of mine from Jack’s days at Wellington., Jack provided the key testimonial for my first book.

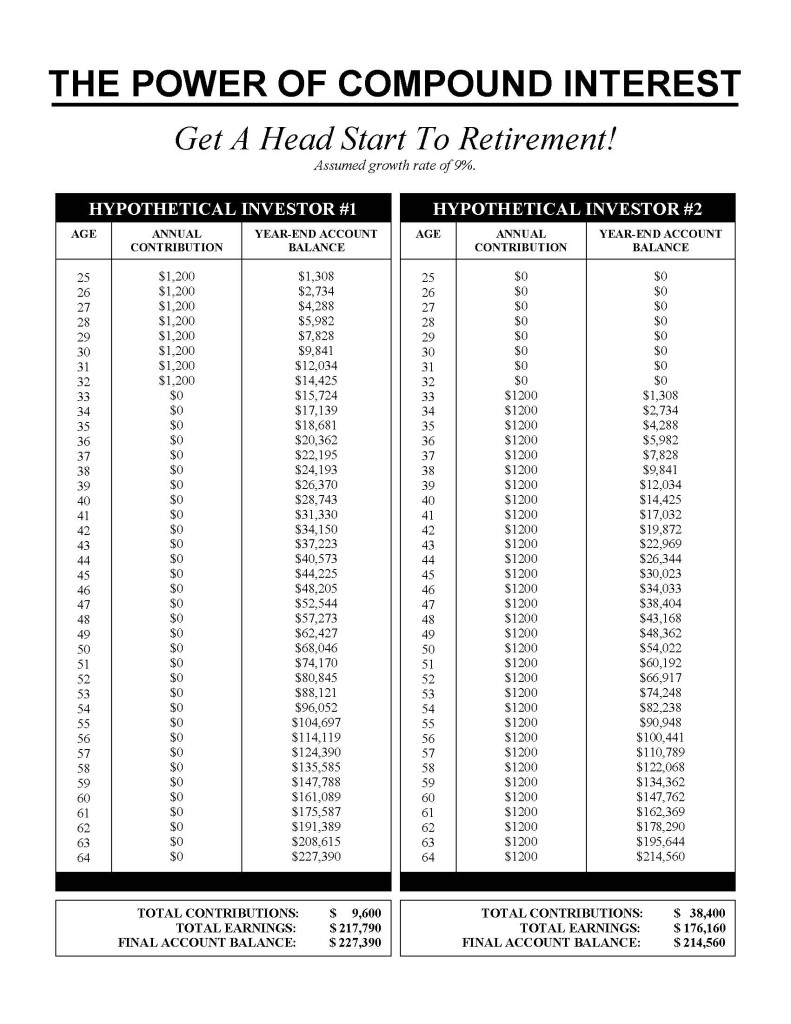

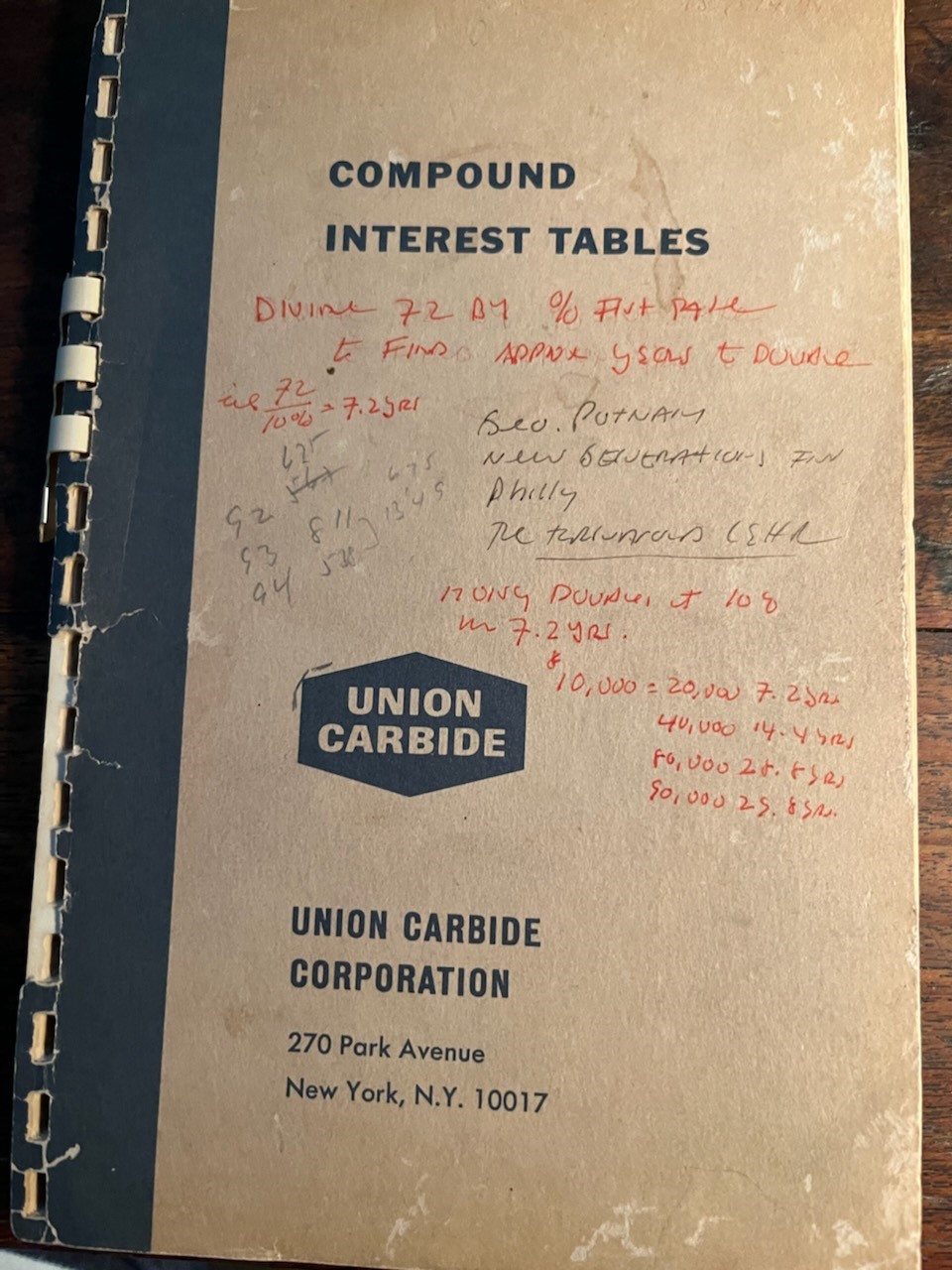

The focus and foundation for my five-decade adventure has been rooted in one little phrase: compound interest. The accompanying photo is my tattered little Union Carbide spiral booklet.

In 1992, Debbie and I bought a little pink Conch cottage in Old Town, Key West, just 90 miles from Cuba. Our son Matt has been our president since, and our daughter Becky is our chief financial officer. E.J. (Your Survival Guy), our son-in-law, after a valued internship with Fidelity, is director of client services.

I continue to research and write seven days a week on behalf of our firm’s clients. Debbie and I still live in Key West, and we do a lot of our research in the 8th arrondissement of Paris. The six-hour time difference works to our favor in getting material to our editorial staff back in Newport, RI.

Thanks to one basic concept – compound interest – I have been able to comfortably and with astounding consistency plot the course for our ultra-conservative, balanced investment firm for over five decades.

You can bet that Debbie and I were pretty proud when our son Matt recently called to tell us that Barron’s had informed him that he had been selected to Barron’s Hall of Fame (2012-2022), while CNBC had just ranked our modest investment management firm #5 in America (2021) out of more than 14,800 registered investment companies. I guess when all is considered, there is a lot of good that be said about compound interest, consistency, and the value of the Prudent Man Rule. Disclosure

As they say, “It works for me.”

Dick Young

Old Town Key West

5 April 2022

90 miles from Cuba