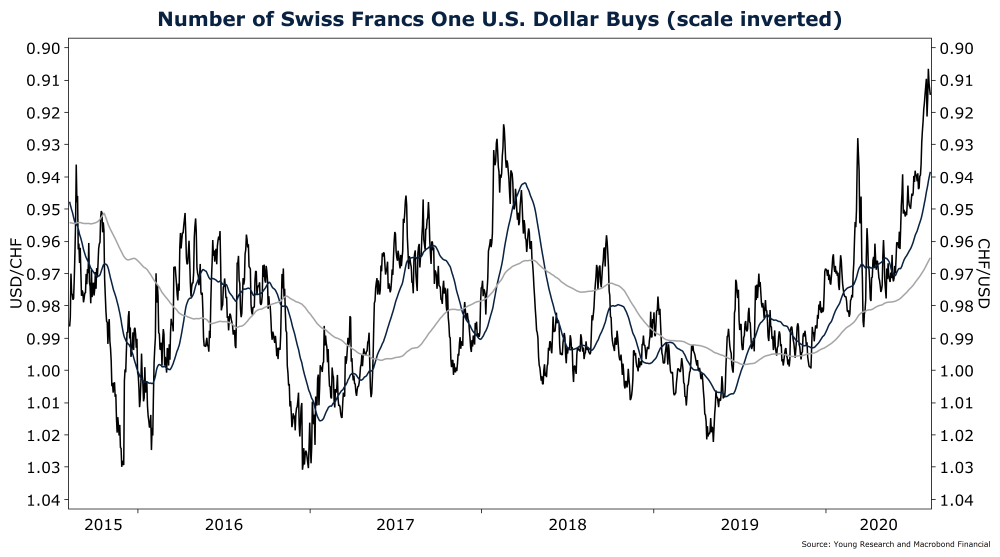

Since last spring, my clients and I have been buying Swiss francs and lately Swiss franc denominated, dividend-paying equities.

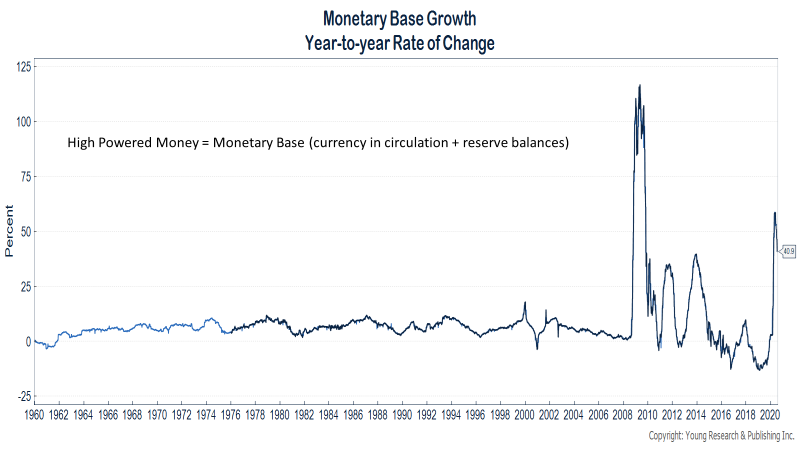

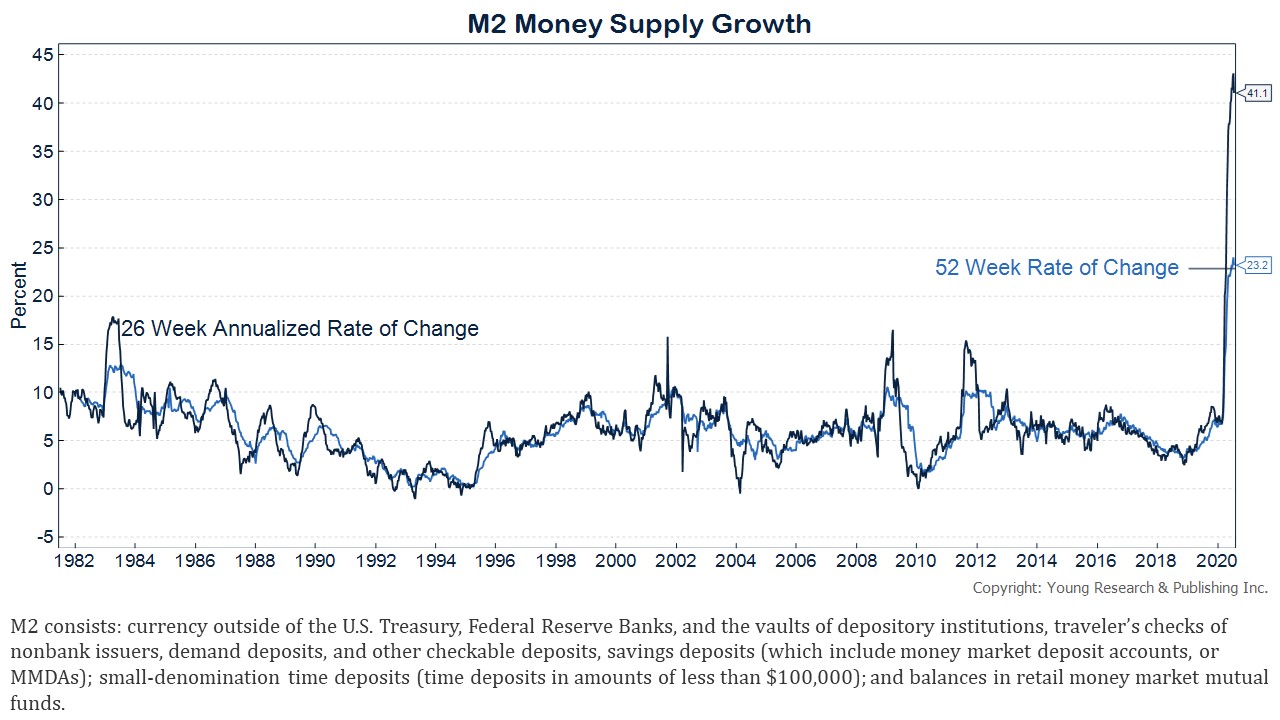

What’s behind the dollar’s collapse? Too many dollars relative to Swiss francs are being printed. It’s no more complicated than that.

It is the Fed who is responsible for debasing the currency.

The Fed’s “private club” was introduced by Woodrow Wilson, America’s worst president, in 1913.

Since then, the Fed has increasingly muddled with the economy in total opposition to its original intent.

I have written often that I would return the Fed to its founding principles prior to shuttering it for good.

In the meantime, the dollar will remain on thin ice.