Thirty years ago this month, I was working hard to explain to investors like you the simple power of having a plan. An investment plan is the reliable engine that keeps your investment train on its track. I told readers they shouldn’t make investments without consulting their plan, writing:

Am I clear on this? Sit back, take a deep breath and repeat after me, “I will have a plan; I will not be a reactionary investor; I will practice diversification.”

Still with me? You see, I want you to lower your financial blood pressure. If an idea is sound today, it must be sound tomorrow. I learned decades ago never to make an investment move on the day I think it is time to move. I always sleep on an idea; rarely am I sorry I’ve waited. Do not be an emotional investor, do not be sold investments by salespeople, and do not make investments that do not fit into your predesigned master plan.

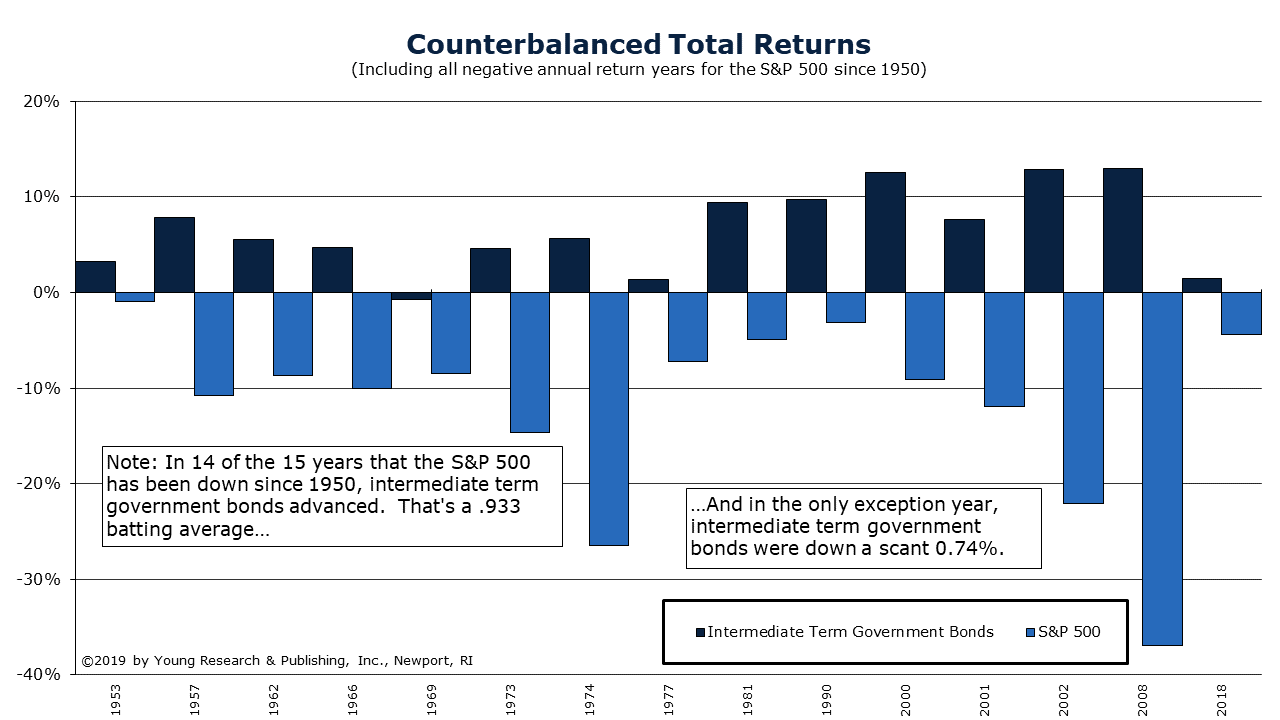

Later I explained how a vital part of my investment plan, diversification, reduces risk, and how important that is to your investment future.

When you own only one stock, your stock portfolio comes with about 72% more risk than the minimum risk, or systematic risk, in owning a portfolio of hundreds of stocks. By simply adding one stock and building a two-stock portfolio, you cut your associated risk to about 36%. By the time you add eight more stocks and reach the 10-position portfolio level, you will have assembled a portfolio that has only about 7% more risk than owning hundreds of stocks. [Editor’s note: For various technical reasons that number is higher today.]

If you are reacting in the investment markets, you’re already too late. You must create a plan ahead of time to deal with market volatility. If you need help building an investment plan, sign up in the form below to be contacted by a seasoned member of the investment team at Richard C. Young & Co., Ltd. They will discuss your financial goals and provide feedback under no obligation.

Act—don’t react.