By Dilok @ Adobe Stock

In The Wall Street Journal, Joseph Sternberg makes the case that the Chinese economy “is in worse shape than you think.” Sternberg notes that China’s economic growth missed the Communist Party’s target. He writes:

You know something is awry in China’s economy when not even the Communist Party can claim things are going according to plan. Witness this week’s economic-growth data for the most recent quarter, which on closer inspection are shockingly bad.

Beijing’s statisticians on Wednesday said the gross domestic product grew 4.3% year-on-year in inflation-adjusted terms in the April through June quarter. China’s economic data are notoriously prone to fiddling for political purposes. And only this March, the Communist Party set a GDP growth target range of 4.5% to 5% for the year, its most pessimistic since the 1990s.

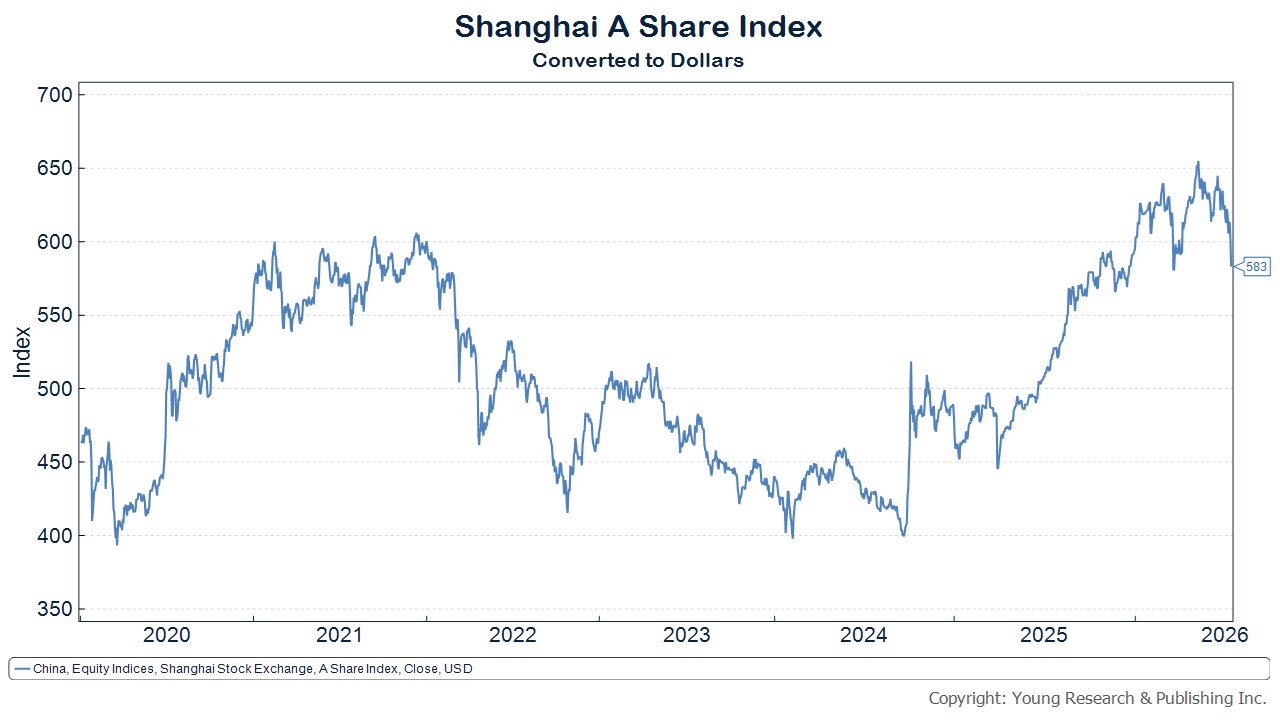

Certainly, the markets are displaying some level of apprehension about Chinese equities. The country’s blue chip CSI 300 Index is down over 10% since its recent peak on June 22.

And the broader Shanghai A Shares Index is down 11% since peaking on May 13th.

Michael Pettis, a Senior Fellow at the Carnegie Endowment, has reported on X.com that Li Daokui, whom Pettis describes as “one of China’s most prominent economists,” is calling for an urgent response to the country’s economic troubles. Pettis writes:

Michael Pettis, a Senior Fellow at the Carnegie Endowment, has reported on X.com that Li Daokui, whom Pettis describes as “one of China’s most prominent economists,” is calling for an urgent response to the country’s economic troubles. Pettis writes:

Tsinghua’s Li Daokui, one of China’s most prominent economists, calls for an increasingly urgent response to problems in the Chinese economy, focusing mainly on policies to unleash constraints on the ability of local governments to continue to power growth: “Specifically, after completing major infrastructure projects, local governments have become preoccupied with repaying their debts. Because interest rates remain high, the more debt they repay, the greater the total debt burden becomes. This process absorbs enormous amounts of economic and financial energy without converting that energy into actual output or productivity.”

His proposed response is to reduce what he calls “blockage” at the local-government level by exploiting the relatively clean balance sheet of the central government. He mostly asks, in other words, for a shift in the locus of debt creation from local-government balance sheets to the central government.

If you believe that there remain a lot of productive investment opportunities that local governments are unable to access because of their bloated balance sheets, and that only local governments can take on these projects, this would certainly make sense.

But I think it has been many years since this has been true, in which case it seems to me that his proposed policy response is to accelerate debt creation even further, partly, he says, to fund local-government repurchases of empty apartments and partly to improve benefits to migrant workers.

My worry is that not enough people see China’s extremely high and rapidly-rising debt burden as the main medium-term problem facing China, perhaps because the only way to address the debt burden requires much slower growth, and as of now this is still politically unacceptable, especially if real Chinese unemployment is closer to the 10.2% Li believes it to be than the 5.0% official rate published earlier today.

It’s good that Chinese economists are becoming increasingly vocal about the deep difficulties the very-unbalanced Chinese economy faces.

But I worry that they are still not willing to acknowledge just how difficult it will be to address these imbalances, nor to recognize that the longer Beijing postpones the adjustment, the more disruptive it is likely to be. On these last two points the historical precedents are pretty clear.

The implications for the rest of the world in response to a sustained bout of slow growth or recession in China are unknown. China hasn’t faced a year of declining GDP since 1976, according to IMF figures. Officially, growth slowed to 2.34% in 2020.