I started in the institutional research and trading investment business at Model Roland & Co. on Federal St. in Boston in August 1971. Just up the street from Model were Fidelity Investments, and Wellington Management, both of whom I called on from my very first hours on the job.

Over five decades ago, Ned Johnson, aka “Mister Johnson,” ran the show at Fidelity. At Wellington, Jack Bogle, “Mr. Mutual Fund,” had not yet left Wellington to start Vanguard.

My focus in the initial going was international research and trading, and remains so today all these decades later. I still consider Fidelity and Wellington the industry leaders.

Both firms feature great cultures, industry-leading technology, well-rounded investment programs for individuals, families, and small businesses–the type of folk I hoped to be associated with throughout my investment career.

Not a business day goes by that one of my associated companies is not involved with one or more of Fidelity or Wellington’s services.

I never would have expected, as I started out in August 1971, that I would be working with Fidelity and Wellington for over 50 years.

In Wellington’s case it, to this day, manages hundreds of billions of dollars in blue-chip, “prudent man rule” quality investment mutual funds.

In the early ’90s, Wellington’s chief investor relations officer informed me that I directed more mutual fund assets Wellington’s way in a given year than did the rest of the combined American investment newsletter industry.

And now in 2025, with our little family investment management company requiring a cutting-edge custodian for our $1.8 billion-dollar conservative Boston-style management company we, not surprisingly, rely on Fidelity.

Your Survival Guy, hard to believe, joined my family business over two decades ago. But before that, he was at Fidelity which he too recalls as being run like a family business. He writes:

When I joined the family business [Fidelity], I was Fidelity employee number twenty-something-thousand. I helped customers/participants of Fortune 500 companies manage their money in this fairly new savings vehicle known by its IRS code: 401(k). It turned out to be a thing. I’ll always remember how CEO Ned Johnson III ran the firm like the family business that it was.

In memos to employees, Mr. Johnson wrote to you as if you were seated around him at the dinner table. Business first, then, after some red wine and dessert (and maybe a piece of dark chocolate for digestion; because he was into taking care of one’s health) he’d leave you with something to think about—like his favored Japanese philosophy Kaizen, meaning constant improvement. Reading his memo in my little cubicle, not at his dinner table, I truly believed that through small steps—like compound interest—I could become the best version of myself. Then it was back to stuffing checks into envelopes.

We need to be reminded of this in times like these. Because when a video game company you typically see at the Mall can stop the market in its tracks, you need to figure out if you’re doing everything you can to protect your money. Are you with an investment company that treats you like a family member? Take a look at the brokerage firms selling their clients’ (I hope not yours) trading patterns to their other customers—these are household names that may (or may not) surprise you. Pay attention.

Action Line: Get your money with a firm that treats you like family. Too many investment firms are profiting from you, for example, with your information without you even knowing it. And don’t get me started on how they use your cash to lend out to others and pocket the profit.

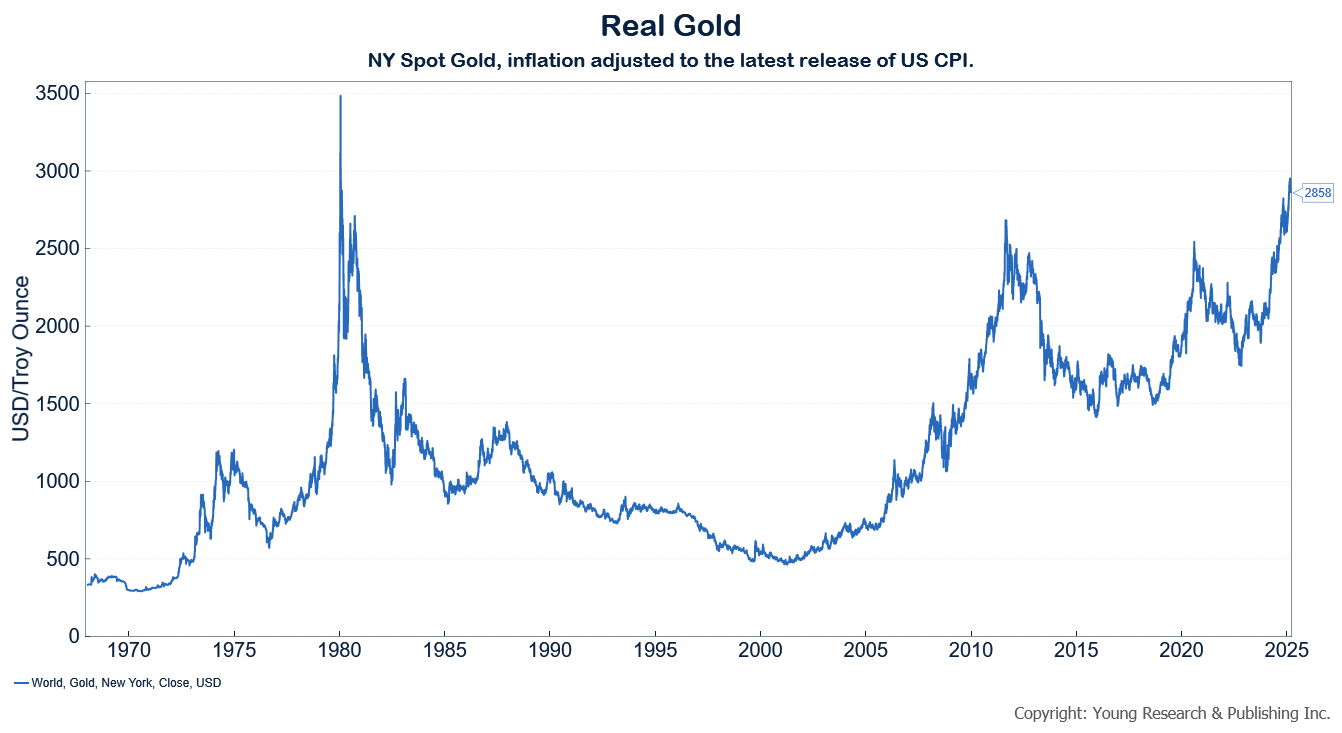

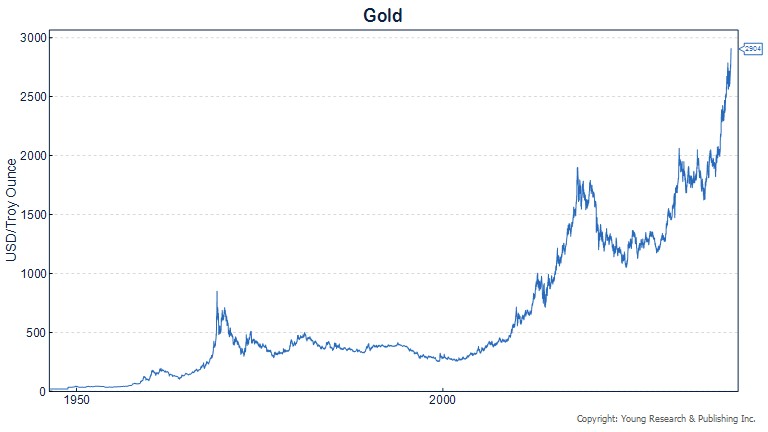

P.S. Read more about how I got my start at Model Roland & Co. back in 1971, and gold’s 50-year price explosion.

Originally posted February 23, 2021.