In my long investment career, nothing has worked harder against my success than the negative compounding effect of inflation. Every year inflation reduces the value of the money I have worked hard to save, and impedes my progress in reaching my investment goals. In March of 2010, I explained to readers the effects of inflation I had seen in my lifetime. I wrote:

Nickels & Dimes

You may have had a similar experience growing up to the one I’m about to tell you. The early 1950s was a great time to be a kid, even more so for me in Cleveland Heights, Ohio, with Paul Brown and Otto Graham leading the Browns.

Often on Saturday afternoon, my brother and I would walk to the movie theater from our house on Birch Tree Path to watch those old-time black-and-white cowboy Westerns featuring Johnny Mack Brown, Tim Holt, Bob Steele, and Ken Maynard. My mom would give us 30 cents each, just right for a Saturday matinee ticket (10 cents), popcorn (10 cents), and a Pepsi (5 cents).

The remaining 5 cents was for Topps baseball cards from the corner store near Noble Elementary. I still have my original collection of Topps baseball cards, albeit sans the colorful wax packaging and the sugardusted pink bubblegum slabs. Topps had just gotten going in the early ’50s and had largely replaced the much better, for my money, Bowman cards.

Savage Inflation

So that’s what 30 cents bought 57 years ago. Today at our super little Tropic Cinema in Old Town Key West, a matinee is $9, popcorn is $3, and Pepsi sells for $2. Baseball cards can run $2.50/pack. In the early ’50s, Pepsi ran a slogan that said, “Twice as much for a nickel, too/Pepsi-Cola is the drink for you.” Pepsi’s large bottles were around even back in the early ’50s. So let’s add it up. $3 + $9 + $2 + $2.50 = $16.50. Depending on where you live, your grand total will be somewhat different from mine. But let’s not quibble. Today we are all paying over 54-to-1 the cost of the early ’50s. That’s some savage inflation and dollar depreciation regardless of how you want to work the math.

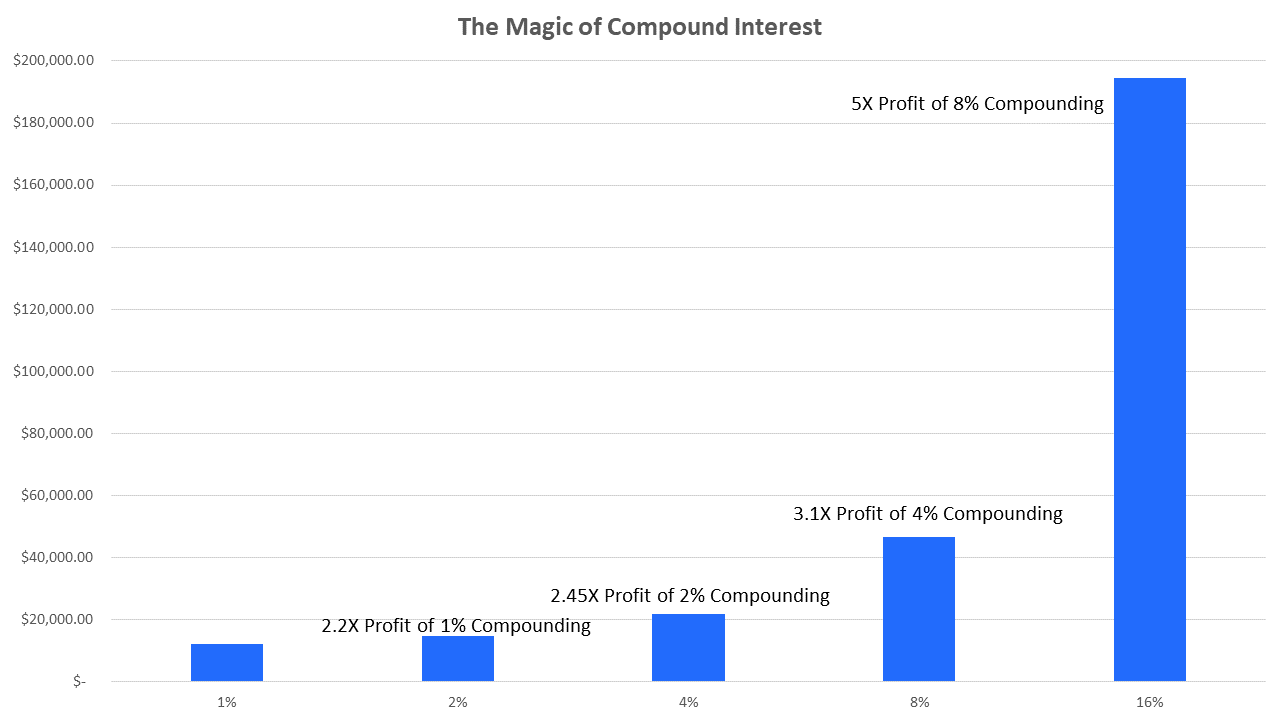

To avoid the savage effects of inflation, I focus my equity investments on companies that not only pay out regular dividends, but also regularly increase those dividends. The steady collection and compounding of such shares can work as an antidote to the poisonous effects of inflation in your portfolio. Make sure you have a plan in place to build an inflation fighting portfolio today.