While you are being transferred to your advisor by the helpful reception staff, you may be put on hold for a brief moment. That’s when you’ll be treated to something I have picked out for you personally. The hold music you’ll hear is a recording of Booker T. and the MGs playing “Green Onions.” Booker T. Jones, recorded his first version of “Green Onions” with the MGs in 1962 after he began composing it two years earlier while still attending high school. “Green Onions” peaked at number 3 on the Billboard Hot 100 in August of 1962 and spent four nonconsecutive weeks at the top of the R&B singles chart.

The first MGs consisted of Lewie Steinberg on bass, Steve Cropper on guitar (a Telecaster), and Al Jackson Jr. on drums. Jones played a Hammond M3 organ on the track. Many will tell you he played a B3, but I have seen the organ with my own eyes at the Stax Museum of American Soul Music in Memphis and can assure you it’s an M3 in the building. This point confuses many because Jones is so well known as a B3 player.

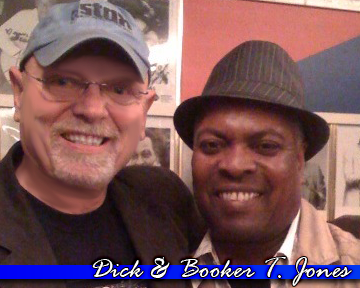

I have followed Booker T. Jones’s career for decades, and I have met him multiple times at venues around the country. When he was inducted into the Musicians Hall of Fame in Nashville in 2008, I was there in the center of the eighth row. I own all of Jones’s original 45s, including multiple versions of “Green Onions,” and play them regularly on my Wurlitzer jukebox at home. The various versions include;

I have followed Booker T. Jones’s career for decades, and I have met him multiple times at venues around the country. When he was inducted into the Musicians Hall of Fame in Nashville in 2008, I was there in the center of the eighth row. I own all of Jones’s original 45s, including multiple versions of “Green Onions,” and play them regularly on my Wurlitzer jukebox at home. The various versions include;

- The original on Stax’s sister label, Volt, released in May 1962, on which Green Onions was the B-side to Behave Yourself.

- A September 1962 release on Stax, with Behave Yourself as the B-side

- And a March 1967 UK-only release on Atlantic Records that included Boot-Leg on the B-Side

The song you hear while you briefly hold during a call to Richard C. Young & Co., Ltd. is not some random muzak assigned to such moments by the telephone company. I picked it out specifically for clients in order to connect them to my lifelong interest in jazz, instrumental R&B, and Southern soul music. There are many versions of “Green Onions,” both by Booker T. himself and others, including an outstanding version by Mike Bloomfield and Al Kooper live at the Fillmore West in 1968. Harry James also recorded a respectable version in 1965.

If you’re looking for investment advice, please call in at 888-456-5444. Enjoy the service you’ll receive, and if you do find yourself on hold, please know that I personally selected the music for you.

Dick Young

P.S. When markets get hit by a hurricane, Young’s World Money Forecast is your port in a storm. Click here to sign up for my free email alert. I’ll never share your information with anyone.