At Young Research, when we look for dividend stocks for the Retirement Compounders, we favor companies with strong balance sheets, stable businesses, a healthy dividend yield, and a history of increasing dividends.

What does that look like in practical terms? While the ideal company financial position for the RCs can vary by industry and sector, Procter & Gamble serves as a nice case study in dividend success.

A Strong Balance Sheet

We look for companies with strong balance sheets because financial strength provides flexibility during tumultuous times in the business cycle.

Procter & Gamble (P&G) has one of the strongest balance sheets among large U.S. businesses. Its debt is rated Aa3/AA- by Moody’s and S&P. Only about 2% of firms in the S&P 500 have a credit rating as good as P&G’s.

P&G’s debt after backing out cash on the balance sheet is about equal to the company’s cash flow before taxes and interest. In other words, P&G could theoretically pay off its debt in a little longer than one year if it used all cash for debt reduction.

With a balance sheet that strong, P&G could fund its dividend for several years even if it runs into a rough patch.

How could P&G fund the dividend during a rough patch? For starters, there is $10 billion in cash on the balance sheet. Assuming a rough patch for P&G caused profit margins to go from 19% today to zero, P&G could fully fund a year’s worth of dividend payments with cash on the balance sheet. The second line of defense for the dividend would be for P&G to borrow money. P&G could easily borrow 2-3 years’ worth of dividend payments without losing its investment-grade rating. Obviously, the definition of a rough patch can vary, but in the scenario outlined above, P&G could have a 3–4-year rough patch without putting the dividend in jeopardy.

Business Stability

P&G’s dividend reliability is also bolstered by the nature of its business. Toilet paper, diapers, toothpaste, and cleaning products are staple purchases for most consumers. That is true whether the economy is in boom or bust. Stable businesses tend to be better equipped for long-term dividend payments and dividend growth than cyclical businesses.

Dividend Payout Ratio

When possible, we also favor companies with modest dividend payout ratios. The payout ratio is the percentage of net earnings paid to shareholders in the form of dividends. Firms with lower payout ratios can more easily continue to pay and raise dividends even during a business downturn. If a company has a payout ratio of 100%, any drop in earnings will either require the company to reduce the dividend because the earnings aren’t there to support it, use cash on hand, or borrow money.

Procter & Gamble pays out about 60% of its earnings to shareholders in the form of dividends. That means earnings could fall by 40% without requiring alternate means to fund the dividend. In practice, for many industries, we compare the dividend to free cash flow instead of earnings to get a truer picture of the payout ratio. P&G looks even better on that metric.

The Dividend

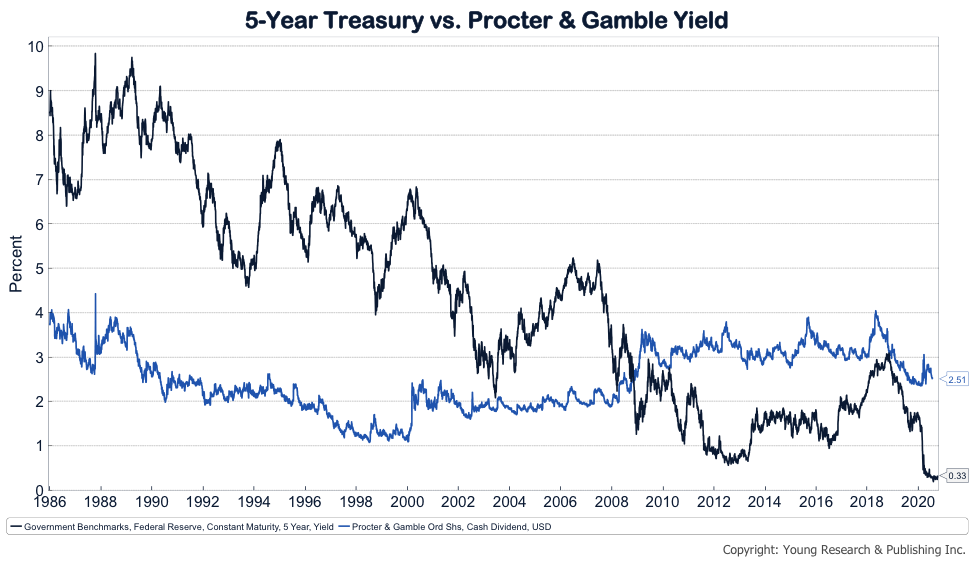

Next is the dividend and the dividend policy. Everything else equal, higher dividend yields are better than lower dividend yields, and a stronger commitment to the dividend in the form of a long record of dividend payments and a long record of dividend increases is better than a weaker commitment to the dividend.

- P&G shares yield 80% more than the S&P 500

- P&G has paid a dividend every year since 1891

- P&G has increased its dividend for 66 consecutive years

The Model of Dividend Success

With a strong balance sheet, a stable business, a modest dividend payout ratio, and an enviable dividend track record, P&G truly is the model of dividend success.