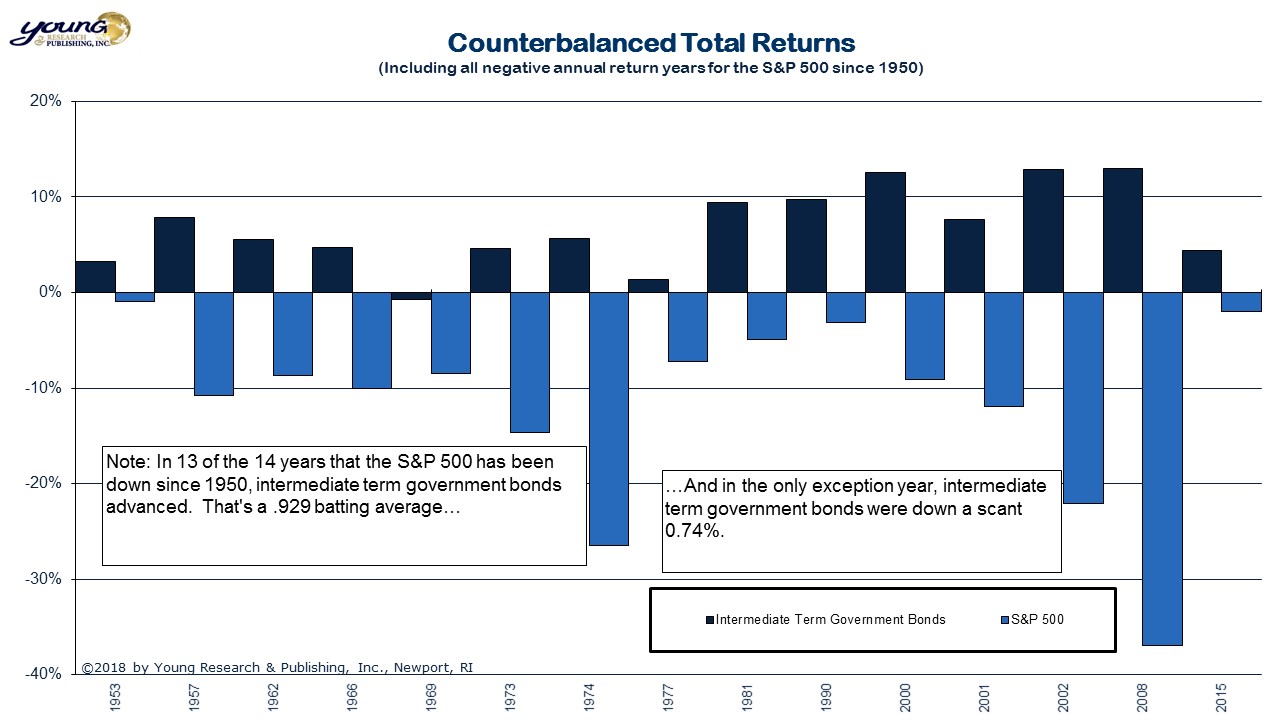

What risks are lurking in your portfolio? Calm markets have made many investors complacent. Are you one of them? Far too many portfolios that come across my desk are heavily invested in risky assets (yes, the S&P 500 counts) with no counterbalancing assets to tame volatility. Look at my chart below to gain an appreciation of just how helpful counterbalancing assets can be in your portfolio.

Here you are looking at the performance of intermediate-term government bonds (dark blue) in years when the S&P 500 (bright blue) lost value. Since 1950, government bonds have been up in 13 of the 14 years that the S&P 500 has been down.

In 1992 I explained to readers a timeless strategy for counterbalancing their portfolios. No matter where you are today in your investment journey, you must address the issue of risk in your portfolio. Read here what I wrote in 1992.

Regardless of your age or ability to take risk, your investment portfolio should be dominated by common stocks (equities) and related open- and closed-end funds on one side, and U.S. Treasury securities and related mutual funds on the other side….

Maintain balance in your portfolio and do not switch back and forth based on your view of the markets. I don’t want you to be an events-of-the-moment shopper. Emotions are difficult to deal with when investing. If you allow emotions and events of the moment to dictate your investment thinking, you will frequently find yourself drawn to do just the wrong thing at just the wrong time in the market cycle. The old buy high, sell low advice lives on.

Designate a fixed percentage of your portfolio for Treasuries and related mutual funds and a fixed percentage for equities. Your age, financial resources, ability to take risk, and need for current income will combine to dictate how you should balance the two. In broad terms, my advice to you is to keep more than half in equities if you are a younger investor, and more than half in 1-10 year Treasuries if you are an ultra-conservative, income-oriented retired investor. Each of you has a different investment profile, so it’s impossible for me to give you precise percentages. Your key is to set down your needs on paper, make yourself address the issue of risk, and then position your portfolio in two parts. Make changes only if your basic investment goals change.

You maintain balance because you do not have a crystal ball. Each day when I buy The Wall Street Journal, I look to see if tomorrow’s date is on the masthead. Unfortunately, it never is, but it does emphasize that neither you nor I ever has tomorrow’s headlines.

It is the unknown that drives the financial markets over the short and intermediate terms (months to quarters). Unless you are a fortune teller, you must accept short- and intermediate-term swings in the markets created by transient and unknown events. You do not want to invest based upon emotions created by events. Instead, invest with an understanding of the long-term principles of earnings, dividends and economic growth that in the end must govern the markets for financial assets.

If you need assistance realigning your portfolio, or if maintaining balance takes too much time and effort, seek help. Firms like my family owned investment advisory service can take the weight of every-day management of your investments off your shoulders. If you want to learn more about the ways a Barron’s Top 100 registered investment adviser (2012-2017) Disclosure is managing risk for its clients, read through the Richard C. Young & Co., Ltd. monthly client letters here. If you wish, you may sign up to receive an alert each time the newest letter is released. The service is free, even for non-clients, so you can easily gain an understanding of our risk management philosophy.

Don’t let inertia hold you back from addressing the risks of unbalanced investments in your portfolio. Act now.