If you are beginning your investment adventure, one of the first questions you may ask yourself is, “how do I diversify my investment portfolio?” Perhaps preceded by, “should I diversify?”

While the answers to how you diversify are many, the answer to whether or not you should diversify is easy; yes, absolutely.

Diversification can lower your risk and raise your returns at the same time. And diversifying can prevent you from feeling the full effects of a downturn in the prices of any single class of assets.

Witness the Raw Power of Diversification

Diversification isn’t only a tool to minimize losses when assets fall in value; it has the power to increase your return while lowering risk. Here’s how I explain it:

Calculating the Efficient Frontier

You need to look at your asset deployment from the top down, focusing on diversification between stocks and bonds. My Efficient Frontier display shows you the power of diversification. Note the left-to-right uphill slanting curve that initiates with a position of 100% bonds and terminates with a position of 100% stocks. We have made our calculations using the Merrill Lynch 7-10 Year U.S. Treasuries Index and the S&P 500 total return index from Young Research for the period of 1977– 2017. We calculate the Efficient Frontier by using annual returns and assuming annual rebalancing.

Draw 1% per Quarter

Where is your best fit along an Efficient Frontier? To answer, you must first establish your ability to absorb risk in the hunt for returns. For decades I have written that in retirement, your target should be a 1% per quarter draw from your portfolio, and not a penny more. This does not mean, however, that you should not position yourself to potentially exceed 1% per quarter returns. Your actual return over any quarter will be controlled largely by the climate of the financial markets at the time, which neither you nor I control. And the climate itself will be determined by the stage of the economic and monetary cycles. I have studied these cycles over five decades and keep you updated regularly. The winter stage of the upside economic and monetary cycle is here, to be followed by a period of discomfort in the economy and the financial markets.

Can You Double Your Money in a Year? Fail at Diversification, and You May Need To

Can you double your money in a year? Not many people can. But if you lost 50% of your portfolio value, that’s precisely what you would need to do to make it back to even.

If the prospect of trying to double your money sounds unappealing, I suggest you try not to lose that much in the first place. I wrote about this a while back, saying:

Unchanged Since the Twenties

According to BBC television, the Classic Coke bottle, the VW Beetle and AGA Cooker are the three finest industrial design achievements of the 20th century. You know the Classic coke bottle, you know the VW Beetle, but the AGA Cooker?

Contemporary stoves pale by comparison to this handcrafted, cast iron cooker that quickly becomes the heart and soul of any kitchen it inhabits. Available in a handful of vibrant enameled color, the heavily insulated, gas-fired AGA has no temperature controls and is always on.

In most kitchens, 80% of cooking is done on the stove top and 20% in the oven. With an AGA, the reverse is true—80% or more is done inside. Externally vented ovens prevent cooking smells from returning to the kitchen, while gentle radiant heat produces superb cooking results—never, ever dried out.

The AGA works on the principle of stored heat within the well-insulated cooker; your job is to simply choose the temperature you want from one of four separate ovens.

This timeless, handcrafted work of beauty, functionality and simplicity was designed over 70 years ago and remains virtually unchanged since the 1920s. For more info on the incomparable AGA Cooker, [visit www.aga-ranges.com].

Timeless describes the AGA’s design, and timeless is the first word I use to describe my investment principles for you. I hope you will embrace my timeless set of investment principles; they will allow you a lifetime of investment rewards.

As a serious, long-term investor, I want you to always consider risk before profits. Never forget, when you lose 50% on an investment, you must double your money next time out just to get even. And even then, you have earned zero return.

Reducing risk in your portfolio is the best way to prevent wild swings that could generate losses from which you can’t come back. Focusing your efforts on diversification, dividends and interest, and on companies in industries with high barriers to entry can help you reduce risk in your portfolio. It’s hard to double your money in a year, but it’s easy to get started on reducing risk in your portfolio.

Build Yourself a Barricade Against Volatility

In the fight to reduce that risk in my portfolio, I remain doggedly attached to my principled investment strategy of diversification and compound interest. I encourage readers to build a “volatility barricade.” I’ve explained my volatility barricade plan before, writing:

Your Volatility Barricade

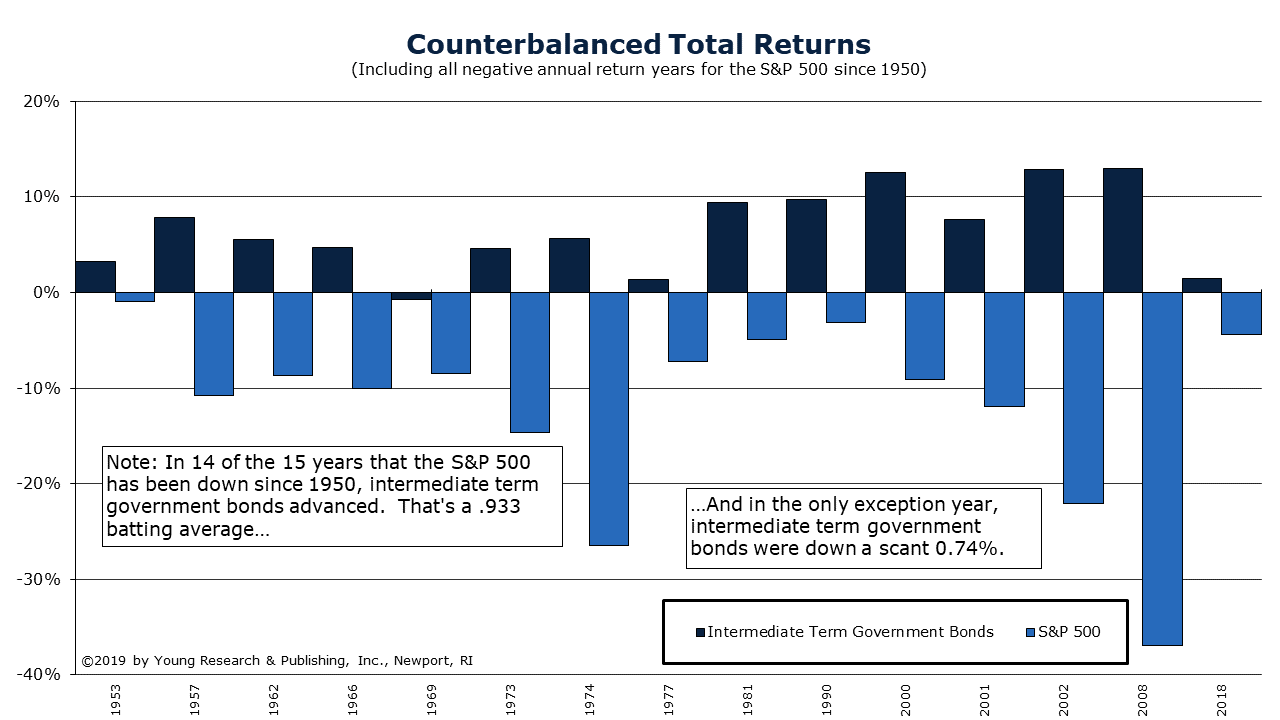

Your portfolio’s fixed-income position does two things for you. (1) It either throws off cash for you to spend at Ace or True Value (not Wal-Mart or Home Depot) in retirement or, instead, allows your interest to compound in an IRA. (2) Your fixed income holdings (short and medium term) will most often zig when stocks zag. You benefit with a counterbalancing teeter-totter. Please [refer to the chart below]. Here you will see that since 1950, in 14 of the 15 years that the S&P 500 has been down, intermediate-term government bonds advanced. That’s a .933 batting average. And in the only exception year, intermediate-term government bonds were down a scant 0.74%. Nice counterbalancing, wouldn’t you say?

If you built yourself a volatility barricade in 2006, you probably withstood the bursting of the housing bubble with fewer gut-wrenching swings in your portfolio’s value than your peers. I encourage every reader to incorporate fixed income into his portfolio today.

Getting on the Map with Gold

Another way I encourage all investors to diversify their portfolios is with a position in precious metals, especially gold.

I have been a longtime supporter of including gold in diversified portfolios. Gold is a safe-haven asset, an inflation and currency hedge, and a hedge against geopolitical turmoil and general market turbulence. It is an insurance policy of sorts. When everything else is down, gold is often up. Gold’s counterbalancing effects can dull the pain of a market rout.

I’ve long been an outspoken advocate of owning gold (I say owning because I buy gold and do not intend to sell). I’ve spoken on gold at conferences around the country, and I have researched and written about gold for nearly 50 years.

Becoming a reliable purveyor of gold insight was no easy trick. At 30 years old I was given a tough, international assignment, and then judged by some of the most demanding names in the business. Here’s the story of the research breakthrough that put me on the gold map.

London, 1971

Portfolio strategy discussions and strategizing with the world’s biggest institutional clients started for me with a mix of Boston, New York, and London research. My institutional research and trading days trace back to August 1971 with Model Roland & Co. The Boston offices were on Federal St. in the old financial district. I was 30 years old.

Gold Research for Leo Model

By the summer of 1972, I was off to London on a gold/gold-shares research trip. This eye-opening experience gave me access and exposure to the largest players in the international gold market. I met contacts and gained background that would be invaluable to me, and thus to my clients, for the ensuing 45 years. Meetings at Samuel Montague and Consolidated Gold Fields, for example, allowed me to craft a detailed report for Leo Model on gold as a commodity as well as a monetary asset.

E.M.B. Comes Through

Mr. Model thought enough of my report to put it into the hands of no less than America’s dean of international monetary experts, Edward M. Bernstein. This was a little unnerving for me as a 30-year old who was prepared for a sour outcome and a lecture from Herr Model, a demanding employer.

Well, much to my surprise, Mr. Model soon received a note from E.M.B., perhaps the #1 expert in the world on the intricacies of gold: “I think the collection of papers on gold is excellent. It seems objective and pointed. I have no suggestions. … Put me on the list to get what Model Roland puts out on gold.”

That did it for me. I was on the map.

Get Your Start Diversifying Your Portfolio Today

These are only some of the ways to diversify your portfolio. You should attempt to diversify as soon as possible. Waiting increases the chances that whichever asset class you are currently invested in will suffer a catastrophic loss.

If you lack the time to understand the complicated process of diversifying your portfolio, you should ask for help. Begin a relationship with one of America’s top investment advisors, like my family run investment counsel firm Richard C. Young & Co., Ltd. Experts there can help you diversify your portfolio across a range of asset classes.

If you would like to speak to a seasoned investment advisor from Richard C. Young & Co., Ltd., for a free, no-obligation portfolio review, please fill out the form below. You will be contacted by someone who can help you navigate the difficulties of diversification.