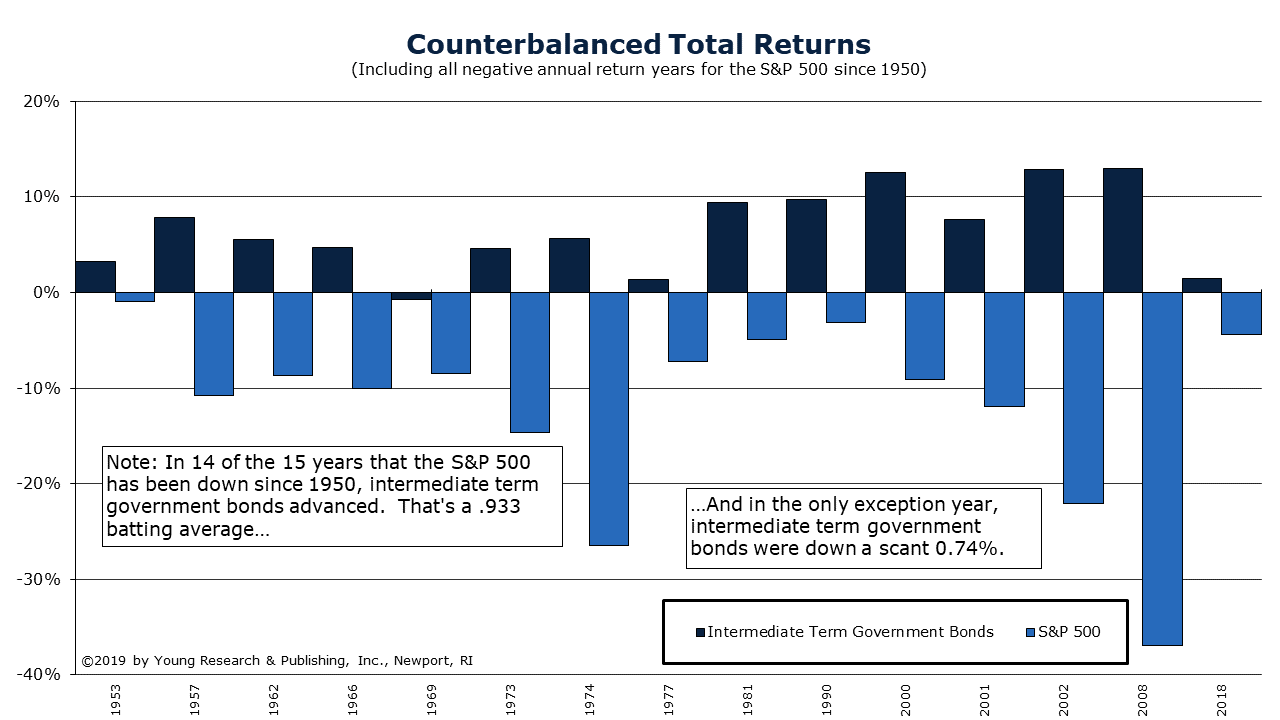

If you have been reading the financial papers or watching CNBC, you have seen the news that the U.S. yield curve has inverted. Typically, this is a sign of a coming recession, and that could be the case today. If, though, you have been following my advice, there is no reason to panic. Have patience and rely on the diversified, counterbalanced portfolio you have built for generating dividends and compound interest. In August of 2013 I explained the power of counterbalancing in your portfolio:

Managing a common stock portfolio takes— above all else—patience. Your goal should never be what to sell next; rather, it should be what stocks you can hold through thick and thin. It is true that portfolio activity, for most investors, runs inversely to consistent long-term performance. How should you measure performance and how should you construct an all-weather portfolio? First, “all-weather” means you do not want to be jumping in and out of the market attempting to predict bull and bear markets. For five decades, I have been investing my own money as well as advising conservative investors saving for retirement. As such, I have invested through many gut-wrenching bear markets and disastrous single years like 2008, which ended with the speculative non-dividend-paying NASDAQ down a frightening 40% for the year. Through all the years of turbulence, I have remained fully invested in a balanced, widely diversified securities portfolio featuring a counterbalanced approach.

I have firsthand experience of what happens when counterbalancing is not in force. The Harleys I rode back in the old days had engines bolted straight to the frame. Talk about vibration and calamity. The constant vibration caused nuts and bolts to loosen and fall off. When you’re on a long-distance road trip, a breakdown in the middle of nowhere is cause for concern. I have found myself in just such a situation and it’s no fun. Today’s Harleys feature counterbalanced engines offering both a smooth ride and a minimum of road trip calamities.

A 2008 Test Kitchen

Counterbalancing simply makes common sense. Let’s look at 2008 as a test kitchen. All the broad averages got hit. High ground, so to say, was achieved by owning positions that got hit least. Consumer staples worked well; no matter how bad the times, investors are not going to forsake toilet paper, toothpaste, or their prescription drugs from Walgreens or CVS.

Counterbalancing is a necessity for your portfolio. If you need assistance in creating a portfolio that is counterbalanced to protect your investments in good times and bad, please fill out the form below. You’ll receive a call from a seasoned investment professional at Richard C. Young & Co., Ltd., my family run investment counsel firm, dedicated to helping retired and soon to be retired investors like you enjoy a successful retirement.